The EROI literature suggests EROI needs to be much higher than 1 to sustain economic growth. Also, some estimates of solar panel (PV) EROI are as low as 3. This short article addresses both of these points: https://www.sciencedirect.com/science/article/pii/S254243511...

See [1] for a more in-depth analysis of this, and much more.

"In America, for example, the benchmark measure of inflation (CPI-U) has been modified by ‘substitution’,

‘hedonics’ and ‘geometric weighting’ to the point where reported numbers seem to be at least six percentage

points lower than they would have been under the ‘pre-tinkering’ basis of calculation used until the early 1980s."

Good comment, except I'd point out that plenty of creativity and invention gets employed in the service of rent-seeking: e.g. most of academic economics, and the way it gets used politically.

Check out Michael Hudson and Richard Werner for a dose of reality.

Brexit aside, some well-informed people are advocating a large Sterling devaluation in order to boost competitiveness [1]:

"We should directly address our lack of competitiveness

by the most obvious and effective means available: by

bringing about a substantial devaluation of the currency."

Well, that's the crux of it right there. You are disagreeing with several authoritative sources who say that no such transfer happens, and in general the loaned funds are created out of thin air.

Standard & Poor's: “Banks lend by simultaneously creating a loan asset and a deposit liability on their balance sheet. That is why it is called credit “creation” – credit is created literally out of thin air (or with the stroke of a keyboard)”

Group of 30: "... banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet."

Richard Werner: "...each individual bank creates credit and money newly when granting a bank loan."

Banks are subject to constraints. They need to retain enough capital to absorb losses on their loan book, and they need to retain enough reserves to cover withdrawals and clearing requirements. They are free to create money "out of thin air" insofar as they meet regulatory requirements associated with those constraints. [1]

You wrote: "I've worked in retail banks and have some hands one (sic) grasp of their day to day operations."

I suggest that your experience does not encompass the whole sector, and that may be the source of your confusion.

OK, how does that gel with a report from S&P [1] that says:

“Banks lend by simultaneously creating a loan asset and a deposit liability on their balance sheet. That is why it is called credit “creation” – credit is created literally out of thin air (or with the stroke of a keyboard)”?

Also Prof Werner's analysis, he reaches the same conclusion.

OK, so if each individual retail bank only lends out pre-existing, deposited funds, where does the increase in the money supply come from? Bear in mind that money created as a by-product of bank lending makes up the vast majority of the total money supply in various modern economies (97% in the UK [1]).

Banks are not merely intermediaries between savers and borrowers. Loans create money, but only loans that are not used to repay other loans result in an increase to the money supply. The following text comes from an ING Bank research note, quoted by The Economist [1]:

"Banks do not view the creation of money as an objective itself. It is a by-product of the banking sector’s business operations. However, it is of great economic and social relevance.

Not every loan ultimately results in new money. The majority of new lending is used to redeem existing loans. Money is only created to the extent the gross lending exceeds the value of the existing loans being redeemed."

That note refers to the "great economic and social relevance" of these banking operations. Here's Professor Richard Werner talking about this at length. [2]

Here's Perry Mehrling (who teaches Coursera's Economics of Money and Banking) weighing in [3]. He explains that it's a nuanced issue but clearly agrees that the "credit creation view" is important and quotes a Group of 30 report:

“In a barter economy, there can rarely be investment without prior saving. However, in a world where a private bank’s liabilities are widely accepted as a medium of exchange, banks can and do create both credit and money. They do this by making loans, or purchasing some other asset, and simply writing up both sides of their balance sheet.”

Governments aren't striving for ideal outcomes - government is necessarily a bunch of scoundrels whose chief goal is to stay in power, which is achieved by giving sufficient bungs to donors and voters:

BTW, you mentioned reservations about possible overspending by Corbyn's Labour. I'm encouraged however by the noises they're making about productivity, e.g. in a recent report:

"The report’s guiding idea is to encourage finance to flow towards productive investment rather than speculation in property. This reflects an old complaint about the City of London: it is a global entrepot with little interest in promoting productive investment in the UK." [1]

And here is a very good primer on the important distinction between productive and unproductive credit. [2]

"Land by its nature is scarce. A site in Mayfair cannot be reproduced like a pair of shoes. The monopoly rent it commands plays no productive role. It acts as a private tax on the productive economy. The question has always been what can be done about it." [1]

I posted that quote because it's the reference I found most speedily to the idea that high land prices impose private (i.e. paid into the private sector) taxation, rather than public. You didn't make the distinction between public vs private taxation in your comment and I thought it should be made.

Public taxation is also involved of course, e.g. when governments need to bail out the banking system; Help to Buy in the UK; etc.

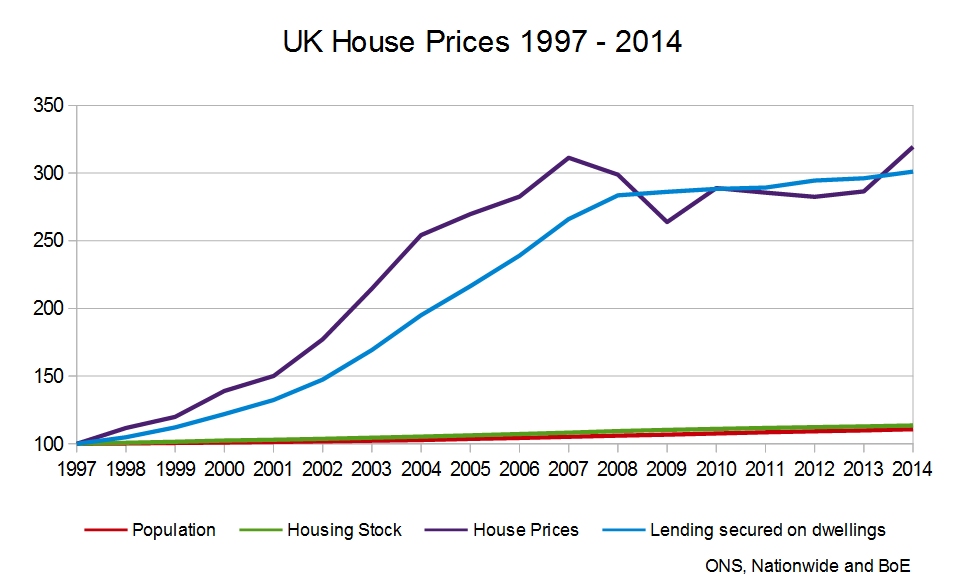

House prices move with mortgage credit growth. Credit growth is one of the key pillars of the politically sustained Ponzi-scheme that is the modern urban housing market.

A major factor affecting housing affordability is the quantity of credit being assigned to mortgages relative to investment in the real economy. This is well explained by a professor of finance here (52 mins): https://youtu.be/N-FDdHj7rPk

Simon Wren-Lewis argues that increasing supply won't help so long as there exists an arbitrage between rental yields and interest rates. Wealthy people will just outbid everyone else for the increased supply: https://mainlymacro.blogspot.com/2018/02/house-prices-and-re...

Richard Werner points out that the mortgage lending, with associated house price inflation, caught fire in the UK after Thatcher eliminated "corset" credit controls. That may be key to sorting the whole mess out.

"Thus the theoretical dream world of “market equilibrium” allows economists to avoid talking about the reality of pervasive rationing, and with it, power being exerted by the short side in every market. Thus the entire power dimension in our economic reality – how the short side, such as the producer hiring starlets for Hollywood films, can exploit his power of being able to pick and choose with whom to do business, by extracting ‘non-market benefits’ of all kinds. The pretense of ‘equilibrium’ not only keeps this real power dimension hidden. It also helps to deflect the public discourse onto the politically more convenient alleged role of ‘prices’, such as the price of money, the interest rate."

Whether Werner supports his own argument adequately is an interesting question. What's not in doubt, to me at least, is that he is in agreement with Harari regarding price discovery being a fiction.

{kind=link}