Value Is Dead, Long Live Value(osam.com)

osam.com

Value Is Dead, Long Live Value

https://www.osam.com/Commentary/value-is-dead-long-live-value

65 comments

> If you look at how companies were being priced, it is clear why value outperformed.

You ought to write a paper. Eugene Fama and Kenneth French have always been pretty upfront about not understanding why value outperforms.

You ought to write a paper. Eugene Fama and Kenneth French have always been pretty upfront about not understanding why value outperforms.

Ford is hovering around a 1.0 price/book ratio and has dropped below that as early as 2018.

Value is still out there. Then as now there are many reasons why people won’t pay more at the present time for these stocks.

Value is still out there. Then as now there are many reasons why people won’t pay more at the present time for these stocks.

If you are measuring value with price/book, you have no hope. The conceit of the "value factor" is wrong-headed: trying to measure value quantitatively is like trying to measure the aesthetic appeal of art quantitatively. It just makes no sense. Quant screens turn up the most uninvestable garbage. The only people who invest that way, haven't ever looked properly at the companies they are investing in (I use value quant screens for shorts now, the flow of money into quant means they are usually comically overpriced).

More to the point though: value is only determined in hindsight. A company trading on 30x earnings can be cheap. The only "value factor" that is closely correlated to returns is 5yr forward earnings. If you think a computer can predict earnings five years forward...great, but they can't.

Also, if you aren't managing $10bn+ you shouldn't be looking at Ford. Don't make it difficult.

More to the point though: value is only determined in hindsight. A company trading on 30x earnings can be cheap. The only "value factor" that is closely correlated to returns is 5yr forward earnings. If you think a computer can predict earnings five years forward...great, but they can't.

Also, if you aren't managing $10bn+ you shouldn't be looking at Ford. Don't make it difficult.

Value investing as Graham and Dodd described it is a very specific strategy. Future earnings are hard to predict or calculate - but factories, land, and cash exist and have real value that is computable.

Right now the market is saying one of two things with a 1.0 price/book:

1) Ford's ongoing business is currently worth $0

OR

2) Ford's capital assets are currently worth $0

It's much easier to make a judgement call on those predicates which are based in the present rather than predict the future.

Right now the market is saying one of two things with a 1.0 price/book:

1) Ford's ongoing business is currently worth $0

OR

2) Ford's capital assets are currently worth $0

It's much easier to make a judgement call on those predicates which are based in the present rather than predict the future.

> Quant screens turn up the most uninvestable garbage.

The markets right now are filled with uninvestable garbage. It's not a value-only thing.

Any viable investment strategy is either a broad based passive investment, or one where you'll have to pick your stocks carefully.

The markets right now are filled with uninvestable garbage. It's not a value-only thing.

Any viable investment strategy is either a broad based passive investment, or one where you'll have to pick your stocks carefully.

I think "Value" is virtually meaningless in modern businesses.

In the past some businesses perhaps depended strongly on capital (e.g. machinery plus cash).

Most modern businesses are simply not dependent on the value of hard capital goods, they depend on the value of their services. The book value of large businesses often contains so many instruments or contracts marked to market, that the book value is largely dependent on market value in disguise.

Examples: TSMC, ARM, a local restaurant, PWC, etc.

Perhaps an exception is real estate companies?

In the past some businesses perhaps depended strongly on capital (e.g. machinery plus cash).

Most modern businesses are simply not dependent on the value of hard capital goods, they depend on the value of their services. The book value of large businesses often contains so many instruments or contracts marked to market, that the book value is largely dependent on market value in disguise.

Examples: TSMC, ARM, a local restaurant, PWC, etc.

Perhaps an exception is real estate companies?

Yes, many value stocks are near the price floor, and have almost no room left to drop further. Of course, some of these companies are that cheap because they are basically the walking dead of companies (e.g. Gamestop). But for the companies that do have a future, now is a good time to invest in them.

You buy stock so you can sell at some future date to convert it into cash. This means you must estimate future value of the stock. The value investing as it gets touted implies that you buy stock given its current value. This is incompatible to the goal of selling stock in future because current value may decline to any arbitrary value. Ford may sell at 1.0 price/book today but it is likely they may to load up on debt down the line OR the value of their assets has lower future value.

So value investing doesn't mean great investing as much as several people wants us to believe. Every stock purchase is necessarily a speculation and there is no escape from that.

So value investing doesn't mean great investing as much as several people wants us to believe. Every stock purchase is necessarily a speculation and there is no escape from that.

> It is particularly foolhardy to place the ending point at 1941.

Seems a perfectly logical point since after that the gov't took control of the economy to fuel the war effort and dictated what was produced.

Also, how may Axis citizens saw high equity returns on their government bonds?

Seems a perfectly logical point since after that the gov't took control of the economy to fuel the war effort and dictated what was produced.

Also, how may Axis citizens saw high equity returns on their government bonds?

It isn't a "perfectly logical point" as I have explained. The study looks at technology, not war (as you are suggesting). It is probably the year in the whole of the century that, in hindsight, explains value returns best...is that coincidental choice? I am not sure what your point is about the Axis either...as with the US and the UK, most people had their savings inflated away.

To be totally clear, and this isn't 100% related with the topic: that period is a terrible example because it is reproducible. The assumption with all these studies of long-term returns is that past returns are reproducible. They are not. If you were a normal citizen around 1941, you were forced to invest in govt bonds (banks were forced to buy govt bonds, if you had a deposit you owned govt bonds).

To be totally clear, and this isn't 100% related with the topic: that period is a terrible example because it is reproducible. The assumption with all these studies of long-term returns is that past returns are reproducible. They are not. If you were a normal citizen around 1941, you were forced to invest in govt bonds (banks were forced to buy govt bonds, if you had a deposit you owned govt bonds).

This overlooks the longterm impact of a new type of company that has been greatly enabled by technology: predatory revenue omnivores. These are companies that have figured out how to identify large revenue flows outside their current business or sector and systematically capture that revenue successfully, over and over (Amazon is a good example). In the past, revenue growth was not sector-agnostic in this way because sector expertise created insurmountable advantages for incumbents such that revenue growth was more a function of sector growth and competition came from within that sector. Attempts to materially expand outside a company's native sector almost always ended in failure. Now it looks like a repeatable business model that a minority of companies have figured out.

More and more, you see alien companies successfully colonizing established sectors and stripping them of their revenue. Few value companies are prepared to handle the scenario when these alien companies show up because historically it has never been a realistic threat. I've seen this play out across several industrial sectors over the last decade and almost without exception, companies retreat to niches that the predator hasn't turned its eyes to yet. That's a strategy for being eaten last. The threat is so far outside their experience that they struggle to see a path forward.

If I was going to invest in "value" these days, I'd invest in the revenue predators. They are going to capture much of the best value revenue eventually but this will give them the appearance of "growth" companies in the short term due to the scale of organic revenue growth this business model creates for them.

More and more, you see alien companies successfully colonizing established sectors and stripping them of their revenue. Few value companies are prepared to handle the scenario when these alien companies show up because historically it has never been a realistic threat. I've seen this play out across several industrial sectors over the last decade and almost without exception, companies retreat to niches that the predator hasn't turned its eyes to yet. That's a strategy for being eaten last. The threat is so far outside their experience that they struggle to see a path forward.

If I was going to invest in "value" these days, I'd invest in the revenue predators. They are going to capture much of the best value revenue eventually but this will give them the appearance of "growth" companies in the short term due to the scale of organic revenue growth this business model creates for them.

It seems like you could instead make an argument that Amazon is just sticking with things they're good at. (Various forms of retail sales, along with cloud computing.) They are not a conglomerate combining unrelated businesses like GE or Berkshire Hathaway.

Lots of expansion within the realms they're in, though.

Lots of expansion within the realms they're in, though.

This is a superficial view of Amazon's business. They increasingly own the upstream manufacturing and production businesses that companies use to produce their products that are then sold retail on Amazon or elsewhere. Amazon isn't just a retailer, they are the supply chain.

Because Amazon is such a powerful force in retail, for businesses that sell on Amazon using Amazon's supply chain to also manufacture their product is the path of least effort. Amazon may not be the cheapest or the best supply chain possible but it is reliable, consistent, and their customer service is good if there is a production problem. Being "hassle-free" is a compelling selling point for many companies, completely independent of the retail considerations.

AWS can be viewed as just a particularly large instance of this but Amazon has been building traditional manufacturing supply chains for their retail vendors for a long time.

Because Amazon is such a powerful force in retail, for businesses that sell on Amazon using Amazon's supply chain to also manufacture their product is the path of least effort. Amazon may not be the cheapest or the best supply chain possible but it is reliable, consistent, and their customer service is good if there is a production problem. Being "hassle-free" is a compelling selling point for many companies, completely independent of the retail considerations.

AWS can be viewed as just a particularly large instance of this but Amazon has been building traditional manufacturing supply chains for their retail vendors for a long time.

> They increasingly own the upstream manufacturing and production businesses that companies use to produce their products

I hadn't heard about this. Where can i read more?

I hadn't heard about this. Where can i read more?

>Amazon is just sticking with things they're good at

>They are not a conglomerate combining unrelated businesses

But they don't and they are. Amazon is monitoring sales of all categories of articles, identifies items that sell well and are easy to knock off, then knocks them off. They held more than 70 private brands in April 2018.

[1] https://www.vox.com/2018/4/7/17208804/amazon-private-label-b...

>They are not a conglomerate combining unrelated businesses

But they don't and they are. Amazon is monitoring sales of all categories of articles, identifies items that sell well and are easy to knock off, then knocks them off. They held more than 70 private brands in April 2018.

[1] https://www.vox.com/2018/4/7/17208804/amazon-private-label-b...

Private-label sales don't seem that different from what other retailers do? Unless they are going into manufacturing?

> will give them the appearance of "growth" companies in the short term due to the scale of organic revenue growth this business model creates for them

That’s not the “appearance” of growth, that seems the definition of growth! I also find your reference to “value revenue” somewhat confusing in the context of the usual growth/value classification of stocks.

That’s not the “appearance” of growth, that seems the definition of growth! I also find your reference to “value revenue” somewhat confusing in the context of the usual growth/value classification of stocks.

I think OP meant “growth” as a category or type of company (as opposed to value companies).

Yes, and they match the definiton of growth stocks as far as I can see. Saying that to invest in "value" (as opposed to "growth") you invest in growth companies like AMZN is quite confusing to me :-)

Edit: For the benefit of those not familiar with the growth/value classification:

Top positions in S&P 500 Value index only (over 1%):

Edit: For the benefit of those not familiar with the growth/value classification:

Top positions in S&P 500 Value index only (over 1%):

APPLE INC

JPMORGAN CHASE & CO

BANK OF AMERICA CORP

UNITEDHEALTH GROUP INC

AT&T INC

CHEVRON CORP

WELLS FARGO

CITIGROUP INC

WALMART INC

INTERNATIONAL BUSINESS MACHINES CO

COSTCO WHOLESALE CORP

MICROSOFT CORP

AMAZON COM INC

ALPHABET INC CLASS A/C

FACEBOOK CLASS A INC

VISA INC CLASS A

MASTERCARD INC CLASS A

CISCO SYSTEMS INC

PFIZER INC

VERIZON COMMUNICATIONS INC

MERCK & CO INC

BOEING

NETFLIX INC

MCDONALDS CORP

ABBOTT LABORATORIES

ADOBE INC

PAYPAL HOLDINGS INC

WALT DISNEY

MEDTRONIC PLC

BERKSHIRE HATHAWAY INC CLASS B

JOHNSON & JOHNSON

EXXON MOBIL CORP

PROCTER & GAMBLE

WALT DISNEY

HOME DEPOT INC

INTEL CORP

COMCAST CORP CLASS A

COCA-COLA

PEPSICO INC

ORACLE CORP

PHILIP MORRIS INTERNATIONAL INC

HONEYWELL INTERNATIONAL INC

ACCENTURE PLC CLASS A[deleted]

Who are these predators? Among FAANG I'd guess only the acquisition of YouTube has been a success, and only modest at best.

Let’s see...

- Apple, Samsung, LG, and Google have supplanted a wide range of consumer products with modern cell phones. Point-and-shoot cameras, some prosumer cameras, low-end document scanners, household telephones, PDAs, small flashlights, small voice recorders, portable tape and CD players, car CD players (via wired or BT connectivity), portable DVD players, boom boxes (via Bluetooth speakers), car GPS navigation systems, compasses (to some extent), pocket notebooks, planners (to some extent), a large segment of the wristwatch and pocket watch market, pocket calculators, professional scientific and graphing calculators, walkie-talkies and handheld radios (not completely though), portable electronic games and some game consoles... those are a few of the big ones.

- There is no type of brick-and-mortar store in any branch of retail or auction that hasn’t been hit hard by Amazon and eBay. Additionally, all the B2B businesses in the retail supply/service chain have been hit hard as either their clients suffer or they themselves lose business to Amazon.

I could go on. The world is a completely different place than what it was 20 years ago.

- Apple, Samsung, LG, and Google have supplanted a wide range of consumer products with modern cell phones. Point-and-shoot cameras, some prosumer cameras, low-end document scanners, household telephones, PDAs, small flashlights, small voice recorders, portable tape and CD players, car CD players (via wired or BT connectivity), portable DVD players, boom boxes (via Bluetooth speakers), car GPS navigation systems, compasses (to some extent), pocket notebooks, planners (to some extent), a large segment of the wristwatch and pocket watch market, pocket calculators, professional scientific and graphing calculators, walkie-talkies and handheld radios (not completely though), portable electronic games and some game consoles... those are a few of the big ones.

- There is no type of brick-and-mortar store in any branch of retail or auction that hasn’t been hit hard by Amazon and eBay. Additionally, all the B2B businesses in the retail supply/service chain have been hit hard as either their clients suffer or they themselves lose business to Amazon.

I could go on. The world is a completely different place than what it was 20 years ago.

While you're not wrong, I don't think all (maybe any?) of these are examples of specifically targeted markets taken over by the companies you mentioned. Apple probably didn't target the flashlight market and decide to take market share from Maglite. I think you've just identified products that have naturally been supplanted by new technologies, many of them falling to the adoption of smartphones. A more appropriate example may be Amazon moving into the groceries market. But even that, one could perhaps argue that their broad market is general retail, with competitors like Walmart and Costco, in which case it wasn't really that far of an extension at all from their natural market. I guess Amazon and Apple moving into the realm of Hollywood and film studios may be a better example. I'd like to see a broader success like Apple taking market share from Automobile manufacturers, etc.

I don't think GP is referring to acquisitions. Acquisitions signal failures of predation. Predation here = putting incumbents out of business. Quickly ramping up to competitiveness in a whole new sector.

An extreme case of "software eating the world," basically.

An extreme case of "software eating the world," basically.

A hallmark of the predators is that they often enter markets without doing any material acquisitions within that sector. They capture revenue organically. This has been reduced to a repeatable system.

That is what makes them so difficult to defend against. They don't behave like market incumbents and they compete with a very different set of skills than are seen in the markets they enter. They also tend to narrowly target the most profitable parts of the sector first instead of the entire value chain and expand from there, which rapidly reduces the profit incumbents could use to invest in a defense.

And in fairness, a lot of sectors are gravy trains for the incumbents. They haven't had to work hard for profits, never mind survival, in a very long time. They also spend the first few years in a state of total denial about the threat when one of these companies shows up.

That is what makes them so difficult to defend against. They don't behave like market incumbents and they compete with a very different set of skills than are seen in the markets they enter. They also tend to narrowly target the most profitable parts of the sector first instead of the entire value chain and expand from there, which rapidly reduces the profit incumbents could use to invest in a defense.

And in fairness, a lot of sectors are gravy trains for the incumbents. They haven't had to work hard for profits, never mind survival, in a very long time. They also spend the first few years in a state of total denial about the threat when one of these companies shows up.

can you give an example of such a predator? how many sectors does Amazon operate in? 2? retail and cloud services. they don't make cars, they don't farm, they don't provide Telecom services, they don't develop real estate. which revenue flows have fallen prey to them? note digital distribution of media (Amazon video and music) is an extension of retail not a different sector. their independent production of said media does count as a wholly new venture but as far as I can tradicional media conglomerates have not fallen prey either.

Amazon, to use that example, is involved in the production supply chain long before products gets to retail. In many verticals, vendors now use Amazon both as an upstream supplier for their production process and a retail channel for the finished product. If you buy a physical book from a major publisher, there is a significant probability that the book was manufactured by Amazon. They have built up all kinds of just-in-time manufacturing facilities and services that supply all kinds of businesses at very competitive rates. These companies are usually not called "Amazon" so you likely don't realize Amazon owns them. In sectors where this has been iterating the longest, it has slowly turned classic industries into IP holding companies that are barely involved in the physical execution of their business.

This is an invisible part of Amazon's business. They've built all manner of manufacturing and production facilities that are further and further up the supply chain. At no point is a business required to retail on Amazon but once you are in their workflow it sure makes things easy for the vendor, and over time Amazon replaces more and more of the supply chain you use.

I've watched this from the inside for the entire lifecycle of Amazon entering a couple different "boring" industries and the process has been as impressive as it has been unstoppable. Amazon is not the only company doing this by any means, they are just the most obvious and there are a few different versions of this strategy.

This is an invisible part of Amazon's business. They've built all manner of manufacturing and production facilities that are further and further up the supply chain. At no point is a business required to retail on Amazon but once you are in their workflow it sure makes things easy for the vendor, and over time Amazon replaces more and more of the supply chain you use.

I've watched this from the inside for the entire lifecycle of Amazon entering a couple different "boring" industries and the process has been as impressive as it has been unstoppable. Amazon is not the only company doing this by any means, they are just the most obvious and there are a few different versions of this strategy.

Print-on-demand is a good example. Do you know any others?

Google has successfully predated most of the traditional publishing and news industry; Netflix has predated film and TV while not quite having the characteristics of either.

Instagram? Twitch? WhatsApp? Github? I know there are more

There are two rational justification for the (seemingly) persistent value factor:

1. It’s just a risk premium. The efficient market hypothesis says that all risk adjusted returns are the same. i.e there is only one Sharpe ratio. Or put another way, there is no excess return without commensurate risk. Using this model, value out performs because of the increased riskiness of the investment. Reward for bearing risk is absolutely persistent so if this first reason is true, it should be persistent forever.

2. Behavioral bias. If this is true, people will wise up and the eventual equilibrium will price value fairly at some point.

Either way, value shouldn’t be able to juice your Sharpe ratio forever. Either the first one is true and the Sharpe ratio is unaffected (just the mean returns, which don’t really matter unless you are unable to access leverage), or value is in fact not persistent, because no behavioral bias can ever be persistent, a priori.

I’m not sure what the answer is, but value alone isn’t worth very much. AQR and other funds usually pair it with factors that have a negative correlation, such as momentum. This allows them to capture significant excess returns, compared to value alone.

1. It’s just a risk premium. The efficient market hypothesis says that all risk adjusted returns are the same. i.e there is only one Sharpe ratio. Or put another way, there is no excess return without commensurate risk. Using this model, value out performs because of the increased riskiness of the investment. Reward for bearing risk is absolutely persistent so if this first reason is true, it should be persistent forever.

2. Behavioral bias. If this is true, people will wise up and the eventual equilibrium will price value fairly at some point.

Either way, value shouldn’t be able to juice your Sharpe ratio forever. Either the first one is true and the Sharpe ratio is unaffected (just the mean returns, which don’t really matter unless you are unable to access leverage), or value is in fact not persistent, because no behavioral bias can ever be persistent, a priori.

I’m not sure what the answer is, but value alone isn’t worth very much. AQR and other funds usually pair it with factors that have a negative correlation, such as momentum. This allows them to capture significant excess returns, compared to value alone.

I'll toss in a third:

3) A rational actor with $1 to their name can't eliminate mispricings because it takes more money than that to move prices. Just because you aren't the first person to show up with knowledge of a mispricing doesn't mean that it has been completely eliminated by the time you get there - those genius hedgefund managers that no mortal can beat may not have enough capital to price every stock in the entire market at exactly what they think it should be.

>unless you are unable to access leverage

It's also worth mentioning that you have to pay for loans. "Organic" risk that comes from buying risky securities doesn't have interest, while "synthetic" risk does.

3) A rational actor with $1 to their name can't eliminate mispricings because it takes more money than that to move prices. Just because you aren't the first person to show up with knowledge of a mispricing doesn't mean that it has been completely eliminated by the time you get there - those genius hedgefund managers that no mortal can beat may not have enough capital to price every stock in the entire market at exactly what they think it should be.

>unless you are unable to access leverage

It's also worth mentioning that you have to pay for loans. "Organic" risk that comes from buying risky securities doesn't have interest, while "synthetic" risk does.

> no behavioral bias can ever be persistent, a priori

Of course it can. Tripping twice over the same stone, etc.

Casinos are full of people playing games with negative expected return after all. And if the stock market is like gambling, it’s mostly on the side of “glamour” (as opposed to “boring”) stocks.

Of course it can. Tripping twice over the same stone, etc.

Casinos are full of people playing games with negative expected return after all. And if the stock market is like gambling, it’s mostly on the side of “glamour” (as opposed to “boring”) stocks.

Well, you would expect the markets to reward the people who didn't have these biases, and hurt the people who still had them. The people with the bias will get poorer and poorer, and the people without it will get richer and richer. Those who get poorer and poorer will increasingly have less influence on the world economy, and those getting richer and richer will have out-sized influence.

Eventually, the pool of suckers will disappear and the market will move onto some other bias to stamp out. You can see this very thing happening in capital markets. I work as a quant and many very simple strategies like value, momentum, quality, etc used to work remarkably well, just 15-40 years ago. Nowadays, you need more sophisticated factors, or combine these simple factors together in unique and interesting ways.

There might be a sucker born every minute, but the sucker will never accumulate enough capital for anyone to ever care about him.

Eventually, the pool of suckers will disappear and the market will move onto some other bias to stamp out. You can see this very thing happening in capital markets. I work as a quant and many very simple strategies like value, momentum, quality, etc used to work remarkably well, just 15-40 years ago. Nowadays, you need more sophisticated factors, or combine these simple factors together in unique and interesting ways.

There might be a sucker born every minute, but the sucker will never accumulate enough capital for anyone to ever care about him.

It's too early to declare that value is dead, a full market cycle will be needed at least.

Looking at the Fama/French HmL series value strongly underperformed growth in the late nineties (the HmL series had a 40% drawdown). The current drawdown is not as large yet (but it's true that it has been going on for over a decade).

"Are Growth and Value Dead?

"1999 was the sixth consecutive year in which the S&P BARRA Growth Index outperformed the Value Index. Some investors have questioned whether Value will ever again be a successful investment approach. Some of them believe this is a “New Era” in which technology stocks are revolutionizing the way business is done: “New Economy” stocks will survive while “Old Economy” stocks (mostly Value stocks) will become extinct."

https://www.northinfo.com/documents/111.pdf

Edit: see also pages 7/8 in https://www.yardeni.com/pub/style.pdf Those charts confirm what I wrote above, growth crushed value 20 years ago but didn't quite kill it...

Looking at the Fama/French HmL series value strongly underperformed growth in the late nineties (the HmL series had a 40% drawdown). The current drawdown is not as large yet (but it's true that it has been going on for over a decade).

"Are Growth and Value Dead?

"1999 was the sixth consecutive year in which the S&P BARRA Growth Index outperformed the Value Index. Some investors have questioned whether Value will ever again be a successful investment approach. Some of them believe this is a “New Era” in which technology stocks are revolutionizing the way business is done: “New Economy” stocks will survive while “Old Economy” stocks (mostly Value stocks) will become extinct."

https://www.northinfo.com/documents/111.pdf

Edit: see also pages 7/8 in https://www.yardeni.com/pub/style.pdf Those charts confirm what I wrote above, growth crushed value 20 years ago but didn't quite kill it...

Current research from AQR seems to suggest that HmL isn't actually a persistent factor, just a behavioral bias without any economic basis (anymore?). Also current research by AQR suggests that that value is more structural, and is a real risk premia.

I don't think anyone really knows whether value is a real risk premia, and if it's reason is structural or not. I think it's possible that many of the classic factors (value, momentum, carry, reversal, quality) are structural and do exist, but it's going to take a little bit more work than just creating a dollar neutral L/S portfolio exposed to E/P or whatever.

If I had to guess, I would say that value is a real risk premia. That's not to say I would have put my money in it for the last 10 years, though..

I don't think anyone really knows whether value is a real risk premia, and if it's reason is structural or not. I think it's possible that many of the classic factors (value, momentum, carry, reversal, quality) are structural and do exist, but it's going to take a little bit more work than just creating a dollar neutral L/S portfolio exposed to E/P or whatever.

If I had to guess, I would say that value is a real risk premia. That's not to say I would have put my money in it for the last 10 years, though..

> Current research from AQR seems to suggest that HmL isn't actually a persistent factor [...] Also current research by AQR suggests that that value is more structural, and is a real risk premia.

I'm lost. HmL is the classic "value" factor (as in the 3-factor model of Fama and French: market, size and value). I don't say that's the best definition possible (clearly it's not) and I know other definitions exist (but HmL has the advantage of being available for a century). For what it's worth, I prefer cash-flow-based metrics and total shareholder yield (dividends + buybacks + debt reduction).

AQR use an improved definition (using data as current as possible) but I don't think it's terribly different: "The bottom line is that while the standard approach to value was a reasonable and conservative choice that has served the field well, it is not the best possible choice."

https://www.aqr.com/Insights/Research/Journal-Article/The-De...

In their latest publication ("Factor Premia and Factor Timing: A Century of Evidence", that I've not yet read) they say:

"We follow simple value measures used in the literature to capture “cheap” versus “expensive” securities within an asset class. For individual equities, we use the book-to-market ratio following Fama and French (1992, 2012) and Asness, Moskowitz, and Pedersen (2013). For global equity indices, we use the aggregate 10-year cyclically-adjusted price-to-earnings ratio CAPE (value-weighted average P/E ratio for all constituent firms in the index)."

I'm lost. HmL is the classic "value" factor (as in the 3-factor model of Fama and French: market, size and value). I don't say that's the best definition possible (clearly it's not) and I know other definitions exist (but HmL has the advantage of being available for a century). For what it's worth, I prefer cash-flow-based metrics and total shareholder yield (dividends + buybacks + debt reduction).

AQR use an improved definition (using data as current as possible) but I don't think it's terribly different: "The bottom line is that while the standard approach to value was a reasonable and conservative choice that has served the field well, it is not the best possible choice."

https://www.aqr.com/Insights/Research/Journal-Article/The-De...

In their latest publication ("Factor Premia and Factor Timing: A Century of Evidence", that I've not yet read) they say:

"We follow simple value measures used in the literature to capture “cheap” versus “expensive” securities within an asset class. For individual equities, we use the book-to-market ratio following Fama and French (1992, 2012) and Asness, Moskowitz, and Pedersen (2013). For global equity indices, we use the aggregate 10-year cyclically-adjusted price-to-earnings ratio CAPE (value-weighted average P/E ratio for all constituent firms in the index)."

Sorry, I mean Big minus Small. My bad! I guess I started associating high with big and low with small!

> As of June 30, 2019, the Russell 1000 Value has underperformed the Russell 1000 Growth by a cumulative -136%,

This is some pretty fishy math right here

This is some pretty fishy math right here

It depends on whether you divide the larger by the smaller, or vice versa. Say X went from 100 to 50, while Y went from 100 to 100. It can be seen as 50% reduction in X's value or 100% underperformance vs Y.

The 100% number is kind of more useful because it is the extra return on the decision to switch to Y back then.

The 100% number is kind of more useful because it is the extra return on the decision to switch to Y back then.

For someone that is not an investor, would someone please explain the difference between growth and value stocks?

My initial guess is that value stocks are underpriced, while growth stocks are priced correctly for current value, but has significant growth potential How close is that?

My initial guess is that value stocks are underpriced, while growth stocks are priced correctly for current value, but has significant growth potential How close is that?

Value investing: you try to come up with an intrinsic valuation of a security and buy if market price is, say, 60% or lower of that valuation. Famous examples: Benjamin Graham, Warren Buffet, Michael Burry.

Growth investing: buy whatever grows (earnings, revenue, even DAU are all flavors of growth investing). VC investing/startup investing is classic growth investing. PG on the topic: http://www.paulgraham.com/growth.html

Growth stocks are usually overpriced because of hype (looking through rose glasses), but can still be good, as the last 10 years shows.

Growth investing: buy whatever grows (earnings, revenue, even DAU are all flavors of growth investing). VC investing/startup investing is classic growth investing. PG on the topic: http://www.paulgraham.com/growth.html

Growth stocks are usually overpriced because of hype (looking through rose glasses), but can still be good, as the last 10 years shows.

Just to throw some data into the mix: the biggest difference is not between growth or value. It's between US and ex-US equities:

https://www.portfoliovisualizer.com/backtest-asset-class-all...

https://www.portfoliovisualizer.com/backtest-asset-class-all...

SubuculumCode4,

the way I think of this is that the price of any stock is related to the value of its expected future earnings. For value stocks, the bulk of that value is in the near term earnings. For growth, the value is in the long term earnings.

The reason that value stocks outperforms growth stocks in the long term is that people think the distress on value is worse than it is, and overestimate how good it will be for a growth stock.

The reason this is different for now, and in 1926-41, is that the growth stocks executed their business model. And value stocks didn’t revert back from distress.

Hope this helps, Chris

the way I think of this is that the price of any stock is related to the value of its expected future earnings. For value stocks, the bulk of that value is in the near term earnings. For growth, the value is in the long term earnings.

The reason that value stocks outperforms growth stocks in the long term is that people think the distress on value is worse than it is, and overestimate how good it will be for a growth stock.

The reason this is different for now, and in 1926-41, is that the growth stocks executed their business model. And value stocks didn’t revert back from distress.

Hope this helps, Chris

https://www.msci.com/documents/1296102/1339060/Factor+Factsh...

"The foundation of value investing is the notion that cheaply priced stocks outperform pricier stocks in the long term."

"Value has several dimensions: the stock price as a multiple of company earnings, price as a multiple of dividends paid, price as a multiple of book value, and other such “ratio descriptors.”

The idea is that investors in aggregate are too optimistic about the stocks with positive outlook (everybody wants them, they get overvalued) and too pesimistic about the stocks with negative outlook (nobody wants them, they get undervalued). In principle, by investing on the stocks that are currently "cheap" (and undervalued in average) you get better returns as they won't do (in average) as bad as discounted by their stock price.

What I described above is the "value factor" (used to classify stocks in the value/growth axis). You can also do "value investing" looking at the fundamentals for a company and making sure that that particular company is undervalued. The factor approach is a systematic way to do that without a detailed analysis for each company: you try to identify the measures that allow you to capture undervalued stocks in average.

"The foundation of value investing is the notion that cheaply priced stocks outperform pricier stocks in the long term."

"Value has several dimensions: the stock price as a multiple of company earnings, price as a multiple of dividends paid, price as a multiple of book value, and other such “ratio descriptors.”

The idea is that investors in aggregate are too optimistic about the stocks with positive outlook (everybody wants them, they get overvalued) and too pesimistic about the stocks with negative outlook (nobody wants them, they get undervalued). In principle, by investing on the stocks that are currently "cheap" (and undervalued in average) you get better returns as they won't do (in average) as bad as discounted by their stock price.

What I described above is the "value factor" (used to classify stocks in the value/growth axis). You can also do "value investing" looking at the fundamentals for a company and making sure that that particular company is undervalued. The factor approach is a systematic way to do that without a detailed analysis for each company: you try to identify the measures that allow you to capture undervalued stocks in average.

Yeah that's a pretty good guess. Growth generally means a company is expensive relative to it's earnings, profits, or book value. Ratios like P/E (price to earnings), and P/B (price to book) can be used to identify/classify a growth company. Higher these ratios, the higher the stocks exposure to "growth".

A value company is the exact opposite, a stock with low ratios. As you might have suspected, value has been clobbered in the last 10 years, and a bunch of Chicago school economists are pissing their pants (Fama, French, etc).

V

A value company is the exact opposite, a stock with low ratios. As you might have suspected, value has been clobbered in the last 10 years, and a bunch of Chicago school economists are pissing their pants (Fama, French, etc).

V

Could it be that we are better these days at more accurate valuation? (e.g. better analytics?)

Certainly the proliferation of alternative data (online news sentiment, satellite imaginary, GPS location data, etc) has made finding those cheap harder to find because they are probably more fairly priced. Buffet has said that he switched his strategy from finding fair companies and a great price to great companies at a fair price, probably because of this increase of transparency. Also, there are fewer public companies today than in the past, due to consolidation or better liquidity in secondary (private) markets.

If we ranked companies by P/E nowadays, and look at the cheapest stuff, it's often not worth buying. We're talking about the garbage companies that no longer can compete anymore. I think this is partially why value in underperforming. It's picking up all of this garbage that is actually fairly valued, and not cheap because people forgot about it.

Funds like AQR do use value, but then often combine it with a factor that has a negative correlation with it, like momentum. Obviously you wouldn't want to combine value and growth (as they should have a close to -1 correlation, depending on how you define it), but adding a factor that has some negative correlation is very powerful. An example of using the combination of these two factors might work like this:

I see a company that looks relatively cheap, but not cheap enough for a value strategy. I think find it has an upward momentum (the price is rising), though only moderately. Alone, neither of these signals would be strong enough for a buy. But together, I might infer that the company is turning itself around and things are going to get better.

If we ranked companies by P/E nowadays, and look at the cheapest stuff, it's often not worth buying. We're talking about the garbage companies that no longer can compete anymore. I think this is partially why value in underperforming. It's picking up all of this garbage that is actually fairly valued, and not cheap because people forgot about it.

Funds like AQR do use value, but then often combine it with a factor that has a negative correlation with it, like momentum. Obviously you wouldn't want to combine value and growth (as they should have a close to -1 correlation, depending on how you define it), but adding a factor that has some negative correlation is very powerful. An example of using the combination of these two factors might work like this:

I see a company that looks relatively cheap, but not cheap enough for a value strategy. I think find it has an upward momentum (the price is rising), though only moderately. Alone, neither of these signals would be strong enough for a buy. But together, I might infer that the company is turning itself around and things are going to get better.

Related: "VALUE INVESTING: BRUISED BY 1000 CUTS"

https://www.gmo.com/americas/research-library/value-investin...

Direct link to PDF: https://www.gmo.com/globalassets/articles/insights/asset-all...

https://www.gmo.com/americas/research-library/value-investin...

Direct link to PDF: https://www.gmo.com/globalassets/articles/insights/asset-all...

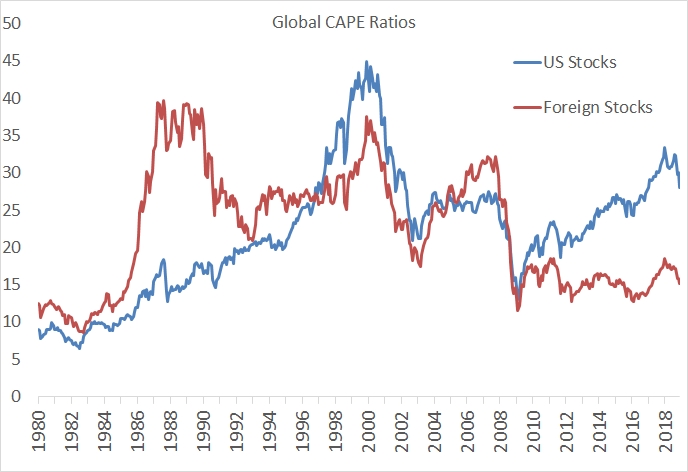

When it comes to value one thing that bugs me is the premium one has to pay for American equities. Like I get it, it's a good market, but it is consistently 30% to 100% more expensive across various metrics. American equities can't be this good.

CAPE is a good case in point here: https://mebfaber.com/wp-content/uploads/2019/01/capeys.jpg

CAPE is a good case in point here: https://mebfaber.com/wp-content/uploads/2019/01/capeys.jpg

{kind=link}

Very well written article from a reputable firm.

Patrick O'Shag's podcast is pretty good too: http://investorfieldguide.com/podcast/

> One should not underestimate the role of regulation in how the Age of Technology plays out.

Yes. The US government needs to step in and enhance privacy and the right to be forgotten... following in the footsteps of our EU brothers.

Patrick O'Shag's podcast is pretty good too: http://investorfieldguide.com/podcast/

> One should not underestimate the role of regulation in how the Age of Technology plays out.

Yes. The US government needs to step in and enhance privacy and the right to be forgotten... following in the footsteps of our EU brothers.

Value has taken a beating for over a decade, and predictably there are pundits crawling out of the woodwork explaining how Warren Buffet's day is long past.

I imagine after the next economic cycle Buffet will again be lauded as a genius.

I imagine after the next economic cycle Buffet will again be lauded as a genius.

He's kind of a closet indexer these days:

https://www.portfoliovisualizer.com/backtest-portfolio?s=y&t...

https://www.portfoliovisualizer.com/backtest-portfolio?s=y&t...

Benjamin Graham was the genius...

Maybe much of the US economy is pointless jobs and pointless economic activity, but the system is viscous enough that the inequilibrium isn't readily apparent.

OT: Is FAANG now used to refer to FAAMA (MS, Alphabet)? I never understood why Netflix was in there with such a small comparative market cap.

Why would anyone think that value investing could ever work? Everyone can easily see the value of a company, because that's a statement about the present, not the future. It's guaranteed to be already priced in when you buy. You will definitely not be the first person to show up after a quarterly is released.

Economists would argue that it is impossible to pickup a $20 from the ground. After all if it was truly a free $20 sitting on the ground then someone else must already picked it up. Thus any $20 sitting on the ground you see must instead be trap.

Part of my growing up has been to realize that sometimes that person picking up the $20 can be yourself. That perfect competition is a theory, and that the world is in fact always far away from that theory. Businesses can survive despite large in-perfections.

Trying to apply efficient market thesis to justify ignoring fundamentals while implicitly claiming growth is not efficiently priced is itself silly. To assume growth is being under priced during an era when all the hype and public attention goes to growth companies is silly.

Boring companies with strong fundamentals and good prices are the vehicles which will preserve wealth and return it to shareholders year in year out. The silly pumps into silly growth companies is the exact behavior marking the end times of a boom cycle.

Part of my growing up has been to realize that sometimes that person picking up the $20 can be yourself. That perfect competition is a theory, and that the world is in fact always far away from that theory. Businesses can survive despite large in-perfections.

Trying to apply efficient market thesis to justify ignoring fundamentals while implicitly claiming growth is not efficiently priced is itself silly. To assume growth is being under priced during an era when all the hype and public attention goes to growth companies is silly.

Boring companies with strong fundamentals and good prices are the vehicles which will preserve wealth and return it to shareholders year in year out. The silly pumps into silly growth companies is the exact behavior marking the end times of a boom cycle.

However it has worked quite well for most of the past century: https://i0.wp.com/thetechieinvestor.com/wp-content/uploads/2...

{kind=link}

Its a risk-based idea.

These companies are valued lower (which everyone sees) because they are thought to be riskier. Theoretically, because less people invest in them because of this, it should result in higher returns for those who stick with the value companies due to the higher risk they are taking on.

The reasoning often goes the other way, academics find a "factor" that outperforms empirically and try to come up with a risk-based explanation backing theoretically what does happen :-)

An alternative explanation is that they are simply mispriced.

An alternative explanation is that they are simply mispriced.

It is particularly foolhardy to place the ending point at 1941. If you didn't know, the period directly after this saw high equity returns because the savings of almost everyone was funnelled by the govt into govt bonds.

If you look at how companies were being priced, it is clear why value outperformed.You had profitable companies with $10 of cash trading for $5. You have companies buying back stock at $10 whilst earning $10. Is this comparable to today?

It is kind of surprising that someone taking the cycle view of history (this is the "hardcore" historian approach) appears to have not looked at any contemporaneous evidence. A theory has been created in hindsight, no evidence from the period has been produced. This is history at its worst, and investment research at its worst. This post should be called: all the things you don't learn in the CFA program.